A small part of the population knows that the "Nobel Prize in Economics" is in fact the "Swedish Central Bank Prize in Economic Sciences in Memory of Alfred Nobel". There are many similarities between the selection for the regular Nobel Prizes and for the Swedish Central Bank Prize in Economic Sciences, and there is indeed a deliberate will to be consistently identified with them.

But only a few persons remember that this Prize in Economics was first awarded in 1969, i.e. 68 years after the regular ones.

Some brief statistics have been published about the laureates, by country in which are located the universities where they worked (cf references). I have updated these results to take into account the years 2011, 2012, 2013 :

Okay, nice shoot from anglo-saxon scholars. Now with such an overwhelming share of first-class thinkers awarded for their achievements during their life-long careers (specially in macroeconomics domain), the U.S. and UK economies should be huge successes, shouldn't they ?

1- Mainstream economists (both Friedman's side and Keynes' side) are always very reluctant to confront their models and their past predictions with long term and updated data series.

Let's just have a look if they really won the match since 1960's :

- How close to an exponential trend is the growth of U.S. Total Public Debt :

Source: Conscience-Sociale.org, using Fed data up to 2013Q1

- How close to an exponential trend is the growth of Federal Total Public Debt (In 2013 Q1, it reached US$ 16.8 Trillion) :

Source: Conscience-Sociale.org, using Fed data up to 2013Q1

- Interest rates in US and UK :

- U.S. Net Export of Goods and Services :

- Real Trade Weighted U.S. Dollar Index :

- Consumer Price Index :

(note the log scale)

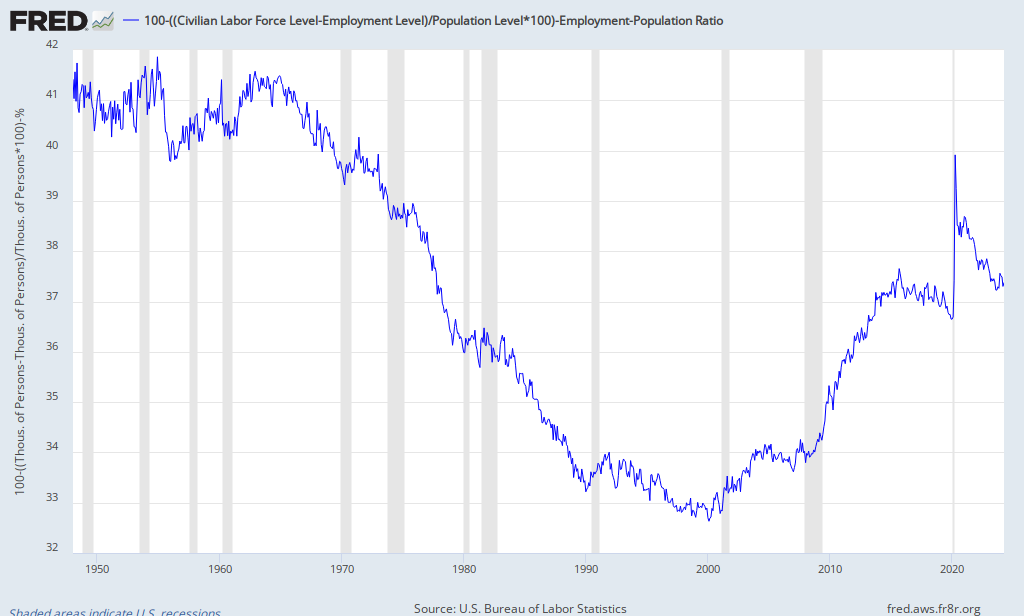

- "Civilian Unemployed and Not Looking Ratio" is the proportion of the civilian non institutionalized population aged 16+ that is unemployed and not looking for work :

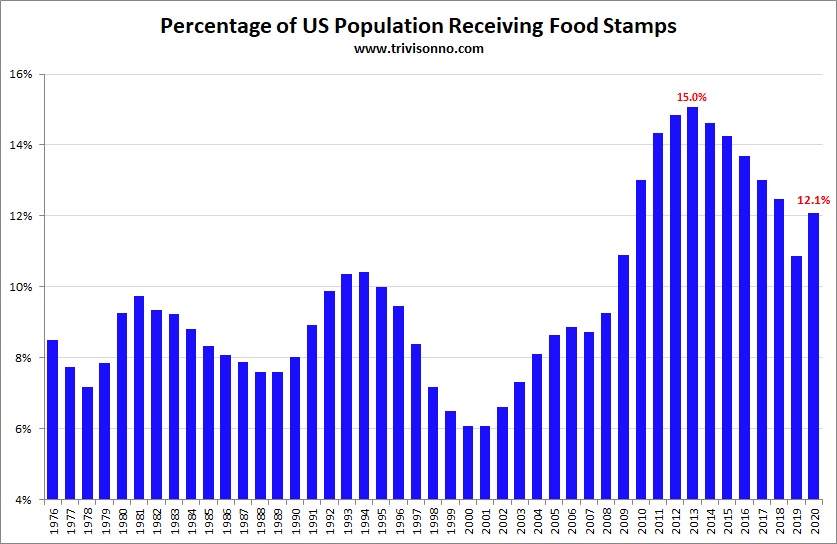

- US Population receiving food stamps :

- Ratio of Corporate dividends over wages & salary :

- There are now more people under “correctional supervision” in America (more than six million) than were in the Gulag Archipelago under Stalin at its height :

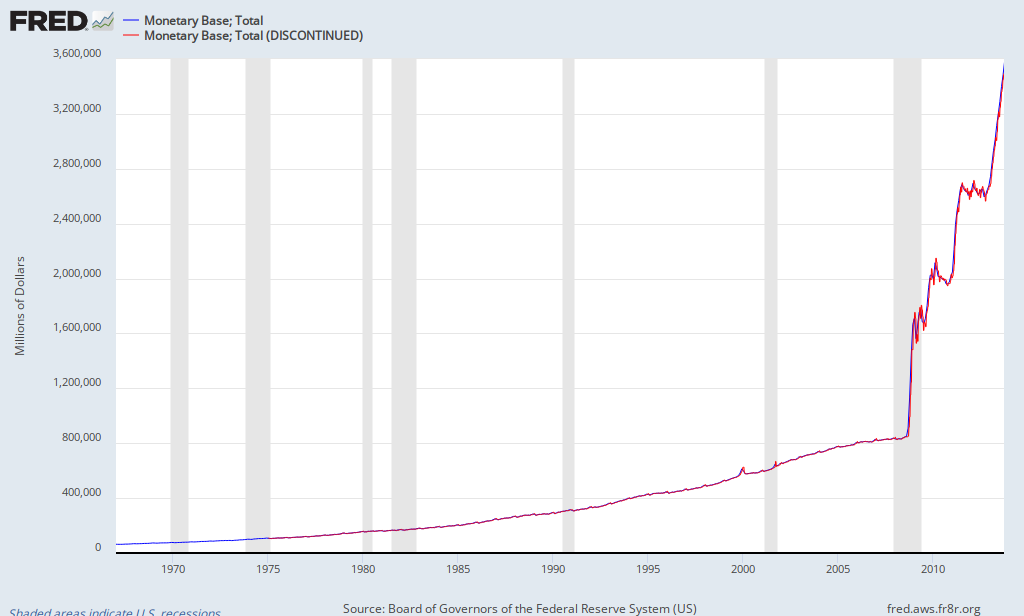

- US total monetary base priced in tonnes of Gold :

- 1 U.S. $ priced in mg of Gold :

- Annual U.S. and UK output produced (GDP per capita) priced in troy ounces of gold :

Source: Conscience-Sociale.org; data series 1791-2012 from MeasuringWorth

2- Observations:

* these results are the worse seen in recorded history.

* The only "positive" result is the historical high and ever rising level of incomes only for the top 1% and above :

* the creation of Nobel memorial Prize in Economics was first announced in 1968, at the same time where neoconservatism in US appeared and neoliberal ideas started to develop.

* all mainstream commentators have analyzed the economical policy of the U.S. and UK to use neoliberals ("Chicago school") principles, and more Keynesian policies since 2008.

* all mainstream commentators have analyzed the economical policy of the U.S. and UK to use neoliberals ("Chicago school") principles, and more Keynesian policies since 2008.

3- Then we can affirm :

- either the US/UK Nobel Memorial laureates in economics were listened by the US/UK governments, but others economists would have given better advices : the observed results prove their Prize was not deserved ;

- or the US/UK Nobel Memorial laureates in economics were listened by the US/UK governments, but others economists would not have been able to give better advices : then the observed results prove economics is still not a science, but only a art. The laureates then deserve an Oscar-like prize, but not a Nobel-like prize ;

- or the US/UK Nobel Memorial laureates in economics were not listened by the US/UK governments, despite the highest level of promotion and audience given, and the observed results prove their Prize was useless and all mainstream commentators were clueless ;

4- In any case, the Nobel Memorial Prize in Economics has proven that deep reforms are required in the way laureates are chosen, at least. Given the historic and catastrophic failure of neoliberalism and therefore the huge loss of credibility of the whole mainstream economics, this will be surely been done.

But given the very low speed of reforms by EU academies, the lock by Swedish Central Bank from one side, and the current global shift of power from the other side, we can anticipate that BRICS will announce the creation of a new "Prize in Economics funded by a BRICS organisation" and elected by the BRICS academies, before any process reform for Nobel Memorial Prize in Economics takes place. This is an anticipated consequence of both the global geopolitical dislocation and the scientific crisis in economics.

We anticipate this announcement within 4 years at the latest, depending on the number of future laureates working in universities located in BRICS countries, or eventually from non mainstream school of economics (for instance A. Fekete from NewASoE but this award alone would finalize a paradigmatic change).

But given the very low speed of reforms by EU academies, the lock by Swedish Central Bank from one side, and the current global shift of power from the other side, we can anticipate that BRICS will announce the creation of a new "Prize in Economics funded by a BRICS organisation" and elected by the BRICS academies, before any process reform for Nobel Memorial Prize in Economics takes place. This is an anticipated consequence of both the global geopolitical dislocation and the scientific crisis in economics.

We anticipate this announcement within 4 years at the latest, depending on the number of future laureates working in universities located in BRICS countries, or eventually from non mainstream school of economics (for instance A. Fekete from NewASoE but this award alone would finalize a paradigmatic change).

The day of this announcement will be the day of the last Nobel Memorial Prize laureate in Economics.

Updated 10/14/2013:

- including results of 2013 awards ;

- My congratulations to Shiller who is pursuing a good work using data and facts about the housing market., although I did not agree with his sale of the rights to build the Case-Shiller index to a private company.

References:

- List of laureates in Economics

- Brief Statistics of the Nobel Prize Winners for Economics, IONECI M., ENE S., 2011; The period observed was 1969-2010.

- The U.S. Debt Dashboard

- Dashboard of US Economy

- The UK Debt Dashboard

- The Gold Basis