Dans la continuité de nos analyses publiées dans le GEAB numéros 100 (12/2015) et 101 (01/2016), voici un nouvel instantané de l'évolution de quelques indicateurs que nous avions mis en lumière. On consultera les numéros du GEAB pour de plus amples explications.

Total of China Foreign Exchange Reserves

source: tradingeconomics.com

Comparez 2015-2016 avec 2008-2009.

Saudi Arabia Central Bank balance sheet in SAR million;

source: tradingeconomics.com

Négatif pour la première fois!

10Y JGB; source: Bloomberg

Y a t'il vraiment un pilote dans l'avion japonais?

30Y JGB; source: Bloomberg

EFSF 10Y; source: tradingeconomics.com

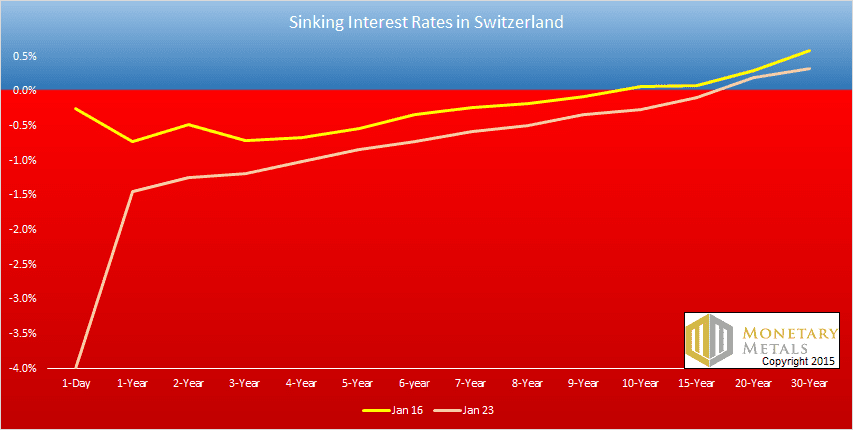

10Y suisse; source: Bloomberg

Et pendant ce temps: retour à la normale de l'économie Russe.

source: tradingeconomics.com